Why MTN Uganda Is a Free Call Option on Fintech’s Future

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Please consult your financial advisor before making any investment decisions. Do your own research.

I wrote this when MTN was initially scheduled to complete the EGM for a vote on a structural separation of the Telcom business from the mobile money business on July 2. The analysis still applies in my view.

This week MTN Uganda shareholders voted on the structural separation of the Telcom business (MTN) from the mobile money business (MTN MoMo).

My thoughts:

1/ Most investors still see MTN Uganda as a mature telco play.

But buried inside it is a high-margin, fast-growing fintech - MTN MoMo - that the market barely values.

Even after the price rally to UGX 261/share, MoMo is still almost free.

And that’s where the real upside lives. I discussed this here.

2/ As of June 30, MTN trades at UGX 261/share, MTN trades at ~UGX 5.85 Trillion market cap.

But the telecom segment alone, using 6.0x EBITDA (a method of valuing businesses using similar comparable companies e.g. Airtel, Safaricom), is worth UGX 9.39 Trillion, implying a value of UGX 418/share (undervalued vs the current share price of UGX 261/share, undervalued by ~UGX 3.54 Trillion).

So MoMo, by implication, which contributes 36% of profits, is valued at just UGX 0.00 to UGX 1.00 Trillion. Reverse calculation shows MoMo is being valued at zero - or possibly negative value due to market uncertainty, discounting, or structural complexity.

3/ Yet MoMo posted, 31 December 2024:

📈 UGX 394B EBITDA

💰 UGX 250B Net Profit

📊 36% of group earnings

MTN MoMo is still being massively discounted. Fair value could be UGX 5 Trillion. based on peer fintech multiple (Wave, Airtel Money) trading at 12.5x EBITDA, sometimes as high as 18x (MTN Group valued its fintech arm at 18x EBITDA in 2024 – implying UGX 7,100B for MoMo).

4/ MTN Uganda = a live, liquid, dividend-paying call option on MoMo.

No expiry

No premium

No time value decay - Do not expire. Do not lose value simply because time passes. Pay dividends while you wait. Can be held indefinitely

Just pure embedded upside

5/ And the unlock is live:

📅 July 2 EGM → Vote on MoMo separation

🎯 Minority holders get 24% of FinCo via a trust

📈 FinCo to list from 2028 (I hope it can be earlier)

More details can be found in the EGM Circular.

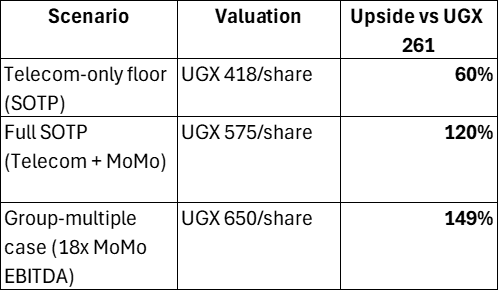

6/ Upside Potential:

Based on a Sum of the Parts (SOTP) valuation:

I think this value can be unlocked faster. I discussed this here.

7/ You don’t get many trades like this:

Defined catalysts

Real floor value

Fintech upside

Embedded call with real cash flows