The AI Bubble, Why Manias Never Really Die (Part 3): Three Red Lights

Subtitle: The Survival Directive has been activated. Here is what the warning lights are saying in April 2026, and what to do about it.

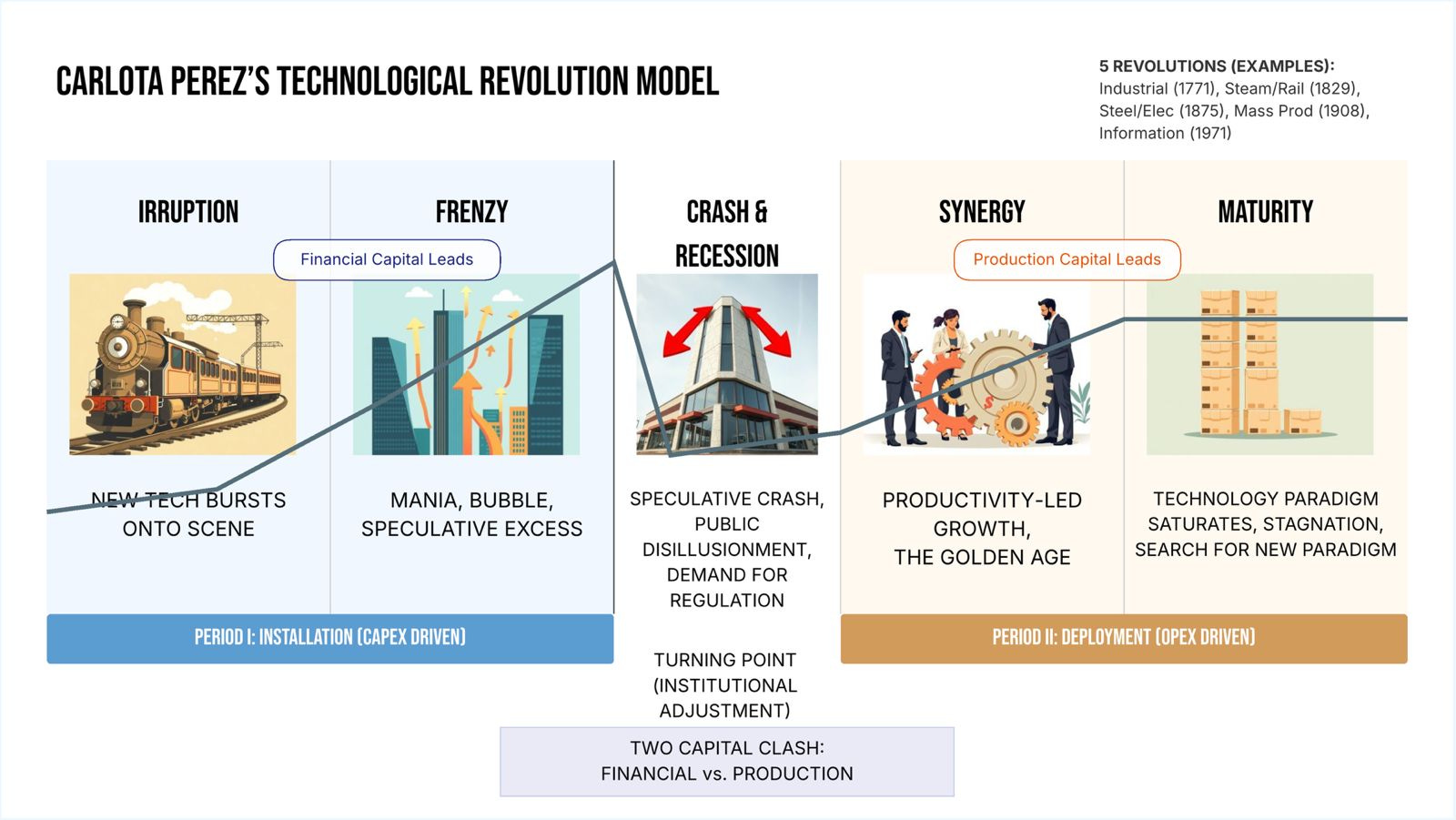

When Part 1 and Part 2 of this series were written, in October and December 2025, the diagnosis was late-frenzy: a market that had overshot fundamentals but had not yet broken down. The framework placed AI squarely in Stage 2 (frenzy) of Carlota Perez’s technological revolution model, with capital flooding the zone faster than the zone could absorb it.

Four months later, the threshold between Stage 2 (frenzy) and Stage 3 (crash and recession) is no longer approaching. It is being crossed — unevenly, node by node, in a way that is simultaneously rewarding disciplined infrastructure positioning and punishing the assumption that all AI stocks move together.

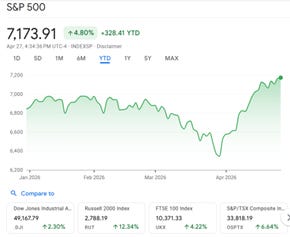

The S&P 500 has returned 4.80% year todate in 2026 while the FTSE All World Index is up 5.8%. And yet the shadow portfolio constructed from the Parts 1 and 2 framework, anchored in AI physical infrastructure, energy, and a 25% liquid ballast returned +36.1% over the same period.

This is not a coincidence. It is the Perez cycle doing exactly what it was described as doing in this series. The physical layer outperforms when the financial layer corrects. The infrastructure endures when the speculation retreats.

“The market is no longer asking how many GPUs you bought. It is asking how much revenue those GPUs generated.” — Bank of America Research, March 2026

The infrastructure build-out is the clearest signal. Capital expenditure has not decelerated, it has accelerated beyond every figure projected prevously. The Big Four are now committed to $635–665 billion in 2026 alone, nearly double 2025’s record levels. Microsoft at $200 billion. Amazon at $200 billion. Alphabet at $175–185 billion. These are numbers that rival the GDP of medium-sized economies, deployed in a single year into physical infrastructure that will not generate its full return for five to seven years.

But the binding constraint is no longer capital or silicon. It is electrons.

A single hyperscale AI training facility now requires 100–300 megawatts of continuous power. The IEA projects global data centre electricity demand will reach 1,000 TWh in 2026, equivalent to Japan’s entire national consumption. Up to 50% of planned data centre projects are stalled waiting for grid connections that are years away.

The bottleneck has migrated from the server rack to the substation. Power, not silicon, now sets the pace.

This Part 3 update covers:

Infrastructure (Node C): The grid is the new bottleneck. Capex has surged to $665 billion combined — but 50% of planned data centres are stalled for power. The full numbers, and what it means for the infrastructure investment thesis.

AI Models (Node A): Open-source has closed the capability gap to roughly three months. OpenAI raised $110 billion at a $730 billion valuation the same week a Chinese model matched it on benchmarks at a fraction of the cost. What this means for the moat thesis.

Application Verticals (Node D): The “Prove It” phase is producing proof — selectively. Coding AI is delivering measurable ROI. Enterprise GenAI spend crossed $37 billion. Physical AI and robotics are still the next decade’s story.

The Five Warning Lights Dashboard: Two of five lights have moved from amber to red since December 2025. The articles defined the threshold: three red lights activates the Survival Directive.

Cycle Position Verdict: A full assessment of where AI markets sit on the Perez diagram today — and the single data point that would most change that assessment.

The full analysis — four original charts, four data tables, the complete Warning Lights dashboard, and the shadow portfolio performance audit follows

The Question the Market Is Now Asking

When Parts 1 and 2 of this series were written, the diagnosis was late-frenzy — a market that had overshot fundamentals but had not yet broken down. The Carlota Perez framework placed AI squarely in Stage 2: capital flooding the zone faster than the zone could absorb it. The articles predicted that 2026–2027 would bring a turning point analogous to 2001–2003.

Four months into 2026, the threshold between Stage 2 and Stage 3 is no longer approaching. It is being crossed, unevenly, node by node. The market is no longer asking “How many GPUs did you buy?” It is asking “How much revenue did those GPUs generate?” That single shift in question is the definition of a turning point.

Two overlapping lenses govern this update. The macro lens is Carlota Perez’s four-stage cycle and the micro lens is the AI Map: four interdependent nodes organising the AI economy. Each node has its own signal. Together, they tell us where we are.

Node C — Infrastructure: The Grid Has Become the Bottleneck

Where are the capex bottlenecks?

Of the four nodes, Infrastructure is where reality has most dramatically diverged from the articles’ projections — not because the build-out has slowed, but because it has accelerated beyond every prior estimate, while simultaneously encountering a constraint that no amount of capital can quickly solve.

The capex numbers:

The articles cited a combined Big Four capex figure of $405 billion for 2025 and projected continued growth. The actuals came in at $392 billion for 2025, but the 2026 guidance has rendered that figure a historical footnote.

Microsoft: ~$97B (2025 Actuals); $120B+ (2026 Guidance); +23–25% (YoY Growth)

Amazon: $131.8B (2025 Actuals); $200B (2026 Guidance); +52% (YoY Growth)

Alphabet: $91B (2025 Actuals); $175–185B (2026 Guidance); +92–103% (YoY Growth)

Meta $72B (2025 Actuals); $115–135B (2026 Guidance); +60–88% (YoY Growth)

Combined: ~$392B (2025 Actuals); $635–665B (2026 Guidance); +62–70% (YoY Growth)

The combined 2026 guidance of $635–665 billion rivals Sweden’s entire GDP. Approximately 75% is directed at AI-specific infrastructure: chips, servers and data centre construction.

The new bottleneck: electrons, not silicon.

The chip shortage of 2021–2024 is no longer the primary constraint. Power availability has replaced silicon as the binding limit on AI expansion. A single hyperscale AI training facility now requires 100–300 megawatts of continuous power.

The IEA projects global data centre electricity demand will reach 1,000 TWh in 2026 — equivalent to Japan’s entire electricity consumption.

The consequences are visible in the development pipeline. Up to 50% of planned data centre projects are stalled waiting for grid connections that are years away. New data centre pipeline additions fell by more than 40% between Q3 and Q4 2025. In Virginia’s Data Centre Alley, communities near major clusters are already reporting electricity rate increases of 8–15%.

This creates a structural irony: the companies committed to spending $200 billion apiece on AI infrastructure are increasingly constrained not by capital or compute, but by the speed at which electrical grids can be upgraded — a process measured in decades, not quarters.

Signal flag: ACCELERATING (capex) / WORSENING (energy — the new primary bottleneck)

Node A — AI Models: The Moat Has Narrowed

Where/How will models evolve?

The articles treated proprietary model providers — OpenAI, Anthropic, Google DeepMind — as commanding durable competitive moats, justified by the extraordinary capital required to train frontier models. That thesis is under pressure from a direction the articles partially anticipated: the rapid compression of open-source capability.

According to Epoch AI, open-weight models now trail state-of-the-art proprietary models by only approximately three months on average benchmark performance. As recently as 2023, that gap was measured in years. The leading open-source models — DeepSeek V3.2, GLM-5, Qwen3 — are approaching or matching proprietary performance on coding, reasoning, and mathematics benchmarks, while running at one to two orders of magnitude lower cost per token.

The private market, however, has not yet priced this compression. In February 2026, OpenAI closed a $110 billion funding round at a $730 billion pre-money valuation — the largest private funding round in history. Anthropic raised $30 billion at $380 billion in the same month. These valuations imply a durable proprietary advantage that the capability data increasingly questions.

Meta, historically the dominant open-source contributor via Llama, is now reportedly developing proprietary frontier models alongside open-source derivatives. Even the open-source champion is hedging toward commercial closure — a signal that the economics of the model layer are in transition, not settled.

Signal flag: ACCELERATING (open-source compression of proprietary moats)

Node B — Data Stack: From Theory to Operational Reality

Is data/context ready — how much?

Enterprise data readiness has crossed from pilots to production for most large organisations, but the nature of the data moat competitive advantage is proving more complex than the standard investment thesis assumed.

According to an Nvidia 2026 State of AI survey, 64% of enterprise respondents are actively using AI in operations, while 28% remain in the assessment phase. Enterprise GenAI spend rose from $1.7 billion in 2023 to an estimated $37 billion in 2025 — a 20x increase in two years.

The data moat thesis, that proprietary training data is an unassailable competitive advantage, is being tested by two simultaneous forces. First, context windows have expanded to 1 million+ tokens on leading models, dramatically reducing the cost of giving the model context at inference time. Second, open-source models fine-tuned on domain-specific data are demonstrating that workflow architecture, not raw data ownership, is where differentiation actually lives.

Signal flag: MODERATING (data moat thesis) / ACCELERATING (enterprise adoption crossing from pilots to production)

Node D — Application Verticals: The Revenue Stack Is Being Built From the Top Down

Which verticals, in what order, are next?

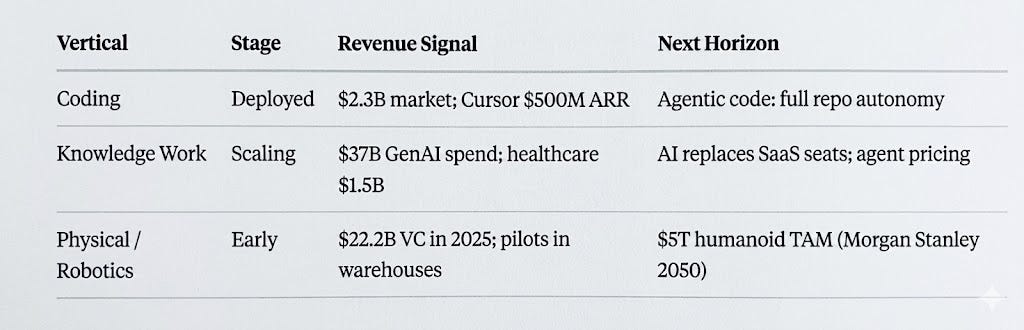

The most important finding in this update is also the most encouraging one for the long-term thesis: the “Prove It” phase is producing proof. Not universally, not at the scale the infrastructure investment implies, but directionally and measurably.

Coding has emerged as the first vertical where agentic AI delivers clear, verifiable ROI. The AI coding tools market has scaled to $2.3 billion in revenue. Leading engineers at OpenAI and Anthropic report that AI now writes the majority — and in some cases virtually all — of their production code.

Physical AI — robotics, autonomous operations — is the next chapter, not the current one. Moving atoms is always harder than moving bits.

Signal flag: CONFIRMED (coding ROI proven) / ACCELERATING (enterprise knowledge work) / EARLY STAGE (physical/robotics)

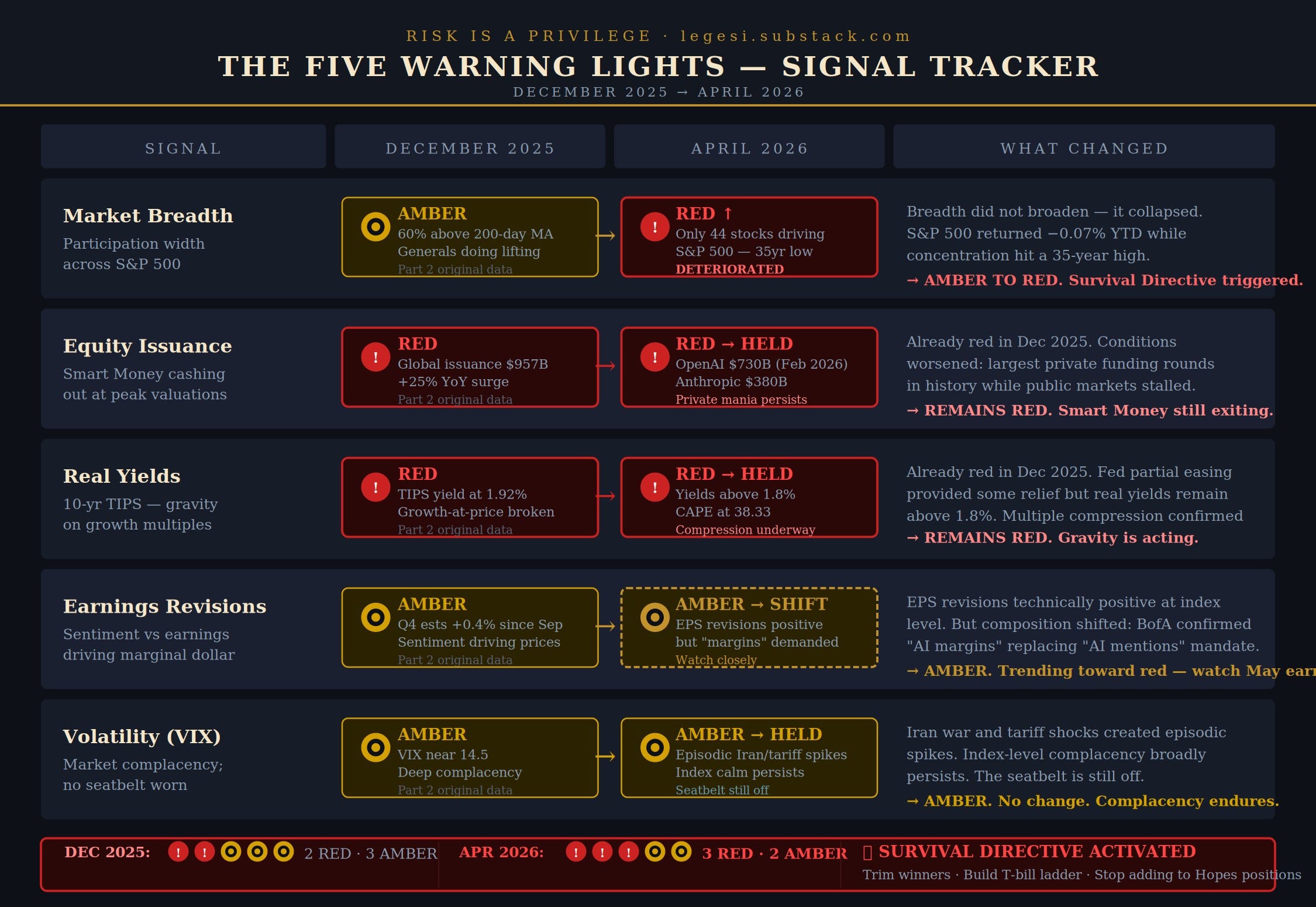

The Five Warning Lights: Current Scoring

Across every speculative cycle — from the South Sea Bubble to dot-coms — the market announces its turning points in roughly the same five ways. We noted in December 2025 that we were seeing all of them, to varying degrees. Four months on, the picture has sharpened.

When Part 2 was published, two of the five lights were already red. That is the baseline that matters. The question for Part 3 is not whether the framework predicted danger — it did, and flagged it explicitly — but whether conditions have deteriorated, stabilised, or in any case improved since December:

In December 2025, the five warning lights read: 2 RED, 3 AMBER. In April 2026, they read: 3 RED, 2 AMBER — with Earnings Revisions shifting from stable amber toward a more uncomfortable zone.

The threshold has been crossed.

Part 2 stated the Survival Directive activates when three or more lights flash red. Market Breadth has now joined Equity Issuance and Real Yields in the red column. The conditions that the articles described as a turning point signal are no longer approaching. They are here.

The directive is clear: shift from offence to defence. Trim positions trading above +2 sigma of their 3-year valuation band. Stop adding to speculative “Hopes” positions at current valuations. Build the T-bill ladder. Preserve the 25% liquid ballast.

This does not mean sell everything. The infrastructure thesis is intact — the physical layer is delivering. What the three red lights say is that the easy money in the broad AI trade is over. What remains is stock selection within a tightening cycle — and patience..

Cycle Position Update: Late-Frenzy to Early Turning Point

Verdict: Late-frenzy is over. The turning point is not coming — it is here.

Four months ago the diagnosis was late-frenzy: fundamentals overshot, but no breakdown yet. The data has moved. Three of five warning lights are now red. The Survival Directive is active. This is no longer a prediction.

The evidence arrives from all four nodes simultaneously.

Infrastructure spent $635–665 billion in 2026 guidance — and hit a wall. Not a capital wall. Not a silicon wall. A power wall. Up to 50% of planned data centre projects are stalled waiting for grid connections. The Stargate campus has reportedly stalled. The bottleneck has migrated from the server rack to the substation, and electrical grids move on decade timelines, not quarterly ones.

Models tell the same story in a different register. OpenAI raised $110 billion at a $730 billion valuation while open-source models closed the capability gap to three months. The moat is narrowing faster than the funding rounds acknowledge.

Verticals are producing proof — selectively. Coding AI is delivering measurable ROI. Healthcare documentation is scaling. Everything else is still finding its footing. The “Prove It” phase has begun producing proof, which is precisely what Stage 3 looks like from the inside: not failure, but the onset of accountability.

Markets have confirmed it in price. The CAPE at 38.33, concentration at 35-year highs, the S&P 500 returning −0.07% while infrastructure names surged. The mandate has shifted from AI mentions to AI margins. Multiple expansion is over. Earnings must now carry the weight alone.

The transition from frenzy to turning point is not a cliff. It is a plateau with a gradient — and we are on it. The technology is real. The infrastructure will endure. But the era of being rewarded simply for showing up in the AI trade is finished.

What remains is stock selection, discipline, and the patience to let the reset complete.

What This Means: The Investor Framework — Updated

The Part 2 framework stands. What changes is the urgency — and the precision — of its application.

Trim the winners. For companies that have triggered the +2 sigma rule, reduce each by 30–40% and redeploy. The framework prescribed the exit on the way up. It prescribes the entry on the way down. Execute both.

Hold the energy infrastructure core. The grid bottleneck is structural. Companies like Eaton, Constellation Energ, and the data centre REITs own the physical constraint no amount of code or capital can quickly solve. Trim the froth. Keep the position.

Deploy the first ballast tranche, selectively. Three red lights are active, but the entry window has narrowed. The S&P 500 closed at 7,177 on April 27 — up 4.85% year-to-date and at a fresh all-time high. While bullish sentiment has recovered above its long-run average for the first time in ten weeks. The structural turning point has not. Deploy 5% of the 25% ballast into names that have not recovered with the index but hold the remaining 20% firm in Cash, T-bills and Gold. A two-week rally does not cancel three red lights.

Capture the rotation. Industrials, healthcare, and consumer staples led while technology lagged. Add non-AI growth, yield curve exposure, and physical infrastructure.

Manias don’t die. They mature. The patient investor who stays solvent through the compression, and positioned correctly for what the infrastructure finances, is the one who wins.

Risk is a Privilege is a newsletter by Kenneth Legesi, CFA. It covers frontier capital markets, AI and Technology, African investment and the macro forces shaping the next decade of investing.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Please consult your financial advisor before making any investment decisions.