Tail Risk: The Losses That Don’t Show Up in Your Models

The case for investing in frontier and emerging markets

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Please consult your financial advisor before making any investment decisions.

Most investors say they understand risk.

What they usually mean is volatility.

They track standard deviation, drawdowns and Value-at-Risk. They debate whether markets are “risk-on” or “risk-off.” They build portfolios designed to survive the next normal shock.

But the losses that shape long-term outcomes rarely come from normal shocks.

They come from tail events, the moments when markets stop behaving like markets. That is tail risk.

What tail risk really is

Tail risk is the risk of rare, extreme events that sit in the far ends of probability distributions and cause disproportionate damage. These are not fluctuations. They are regime breaks.

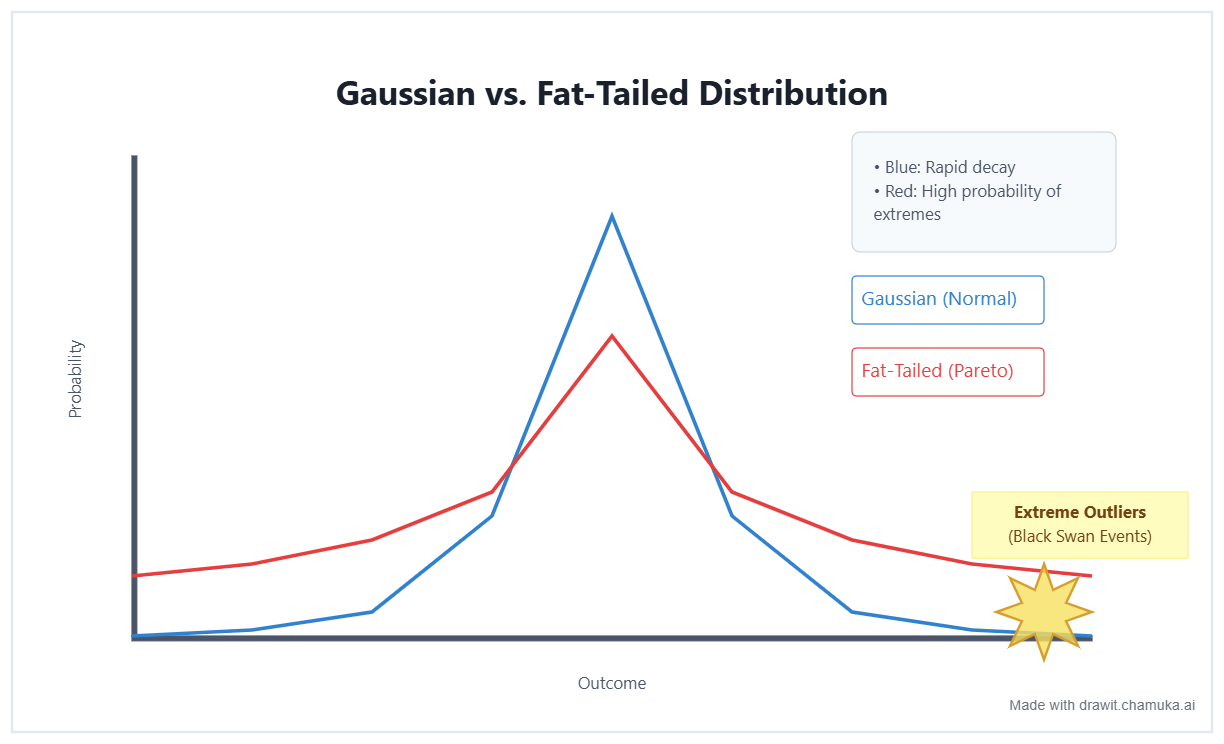

To visualize tail risk, refer to the image above, imagine a standard bell curve (normal distribution) representing investment returns. Most outcomes cluster in the center, the “predictable” fluctuations. Tail risk lives in the thin, elongated edges of that curve.

Tail risk has the following features:

The Probability Illusion: In a “normal” market, the odds of a 6-sigma event (a massive crash) are statistically negligible. However, in frontier markets, these “tails” are often “fat” (leptokurtic). This means extreme events happen far more frequently than standard models predict.

The Impact Gap: While 95% of market movement is “noise” that a portfolio can absorb, the 5% in the tail represents systemic failure such as: a sudden debt restructuring after years of fiscal calm; a surprise currency devaluation that wipes out a decade of equity returns; Capital controls that trap foreign investors overnight; a political rupture that suspends contracts rather than renegotiates them.

Predictability: Fluctuations are priceable; tail risk is not. You can calculate the volatility of the Kenyan Shilling, but you cannot easily “price” the tail risk of a sudden constitutional suspension in a “tranquil” neighbor.

These are not risks that show up cleanly in spreadsheets.

Why tail risk is mispriced

The modern investment industry is built on the assumption that the future will resemble the past closely enough for statistics to be useful. That works until it doesn’t.

Volatility models are excellent at describing what usually happens.

They are terrible at capturing what matters most when it happens least often.

Tail events dominate long-term performance not because they are frequent, but because:

they are large, and

they compound through time.

One unanticipated tail event can erase years of careful optimisation.

The difference between volatility and tail risk

Volatility is noise. Tail risk is fracture.

You can have:

High volatility, low tail risk: noisy markets where institutions absorb shocks and prices recover.

Low volatility, high tail risk: calm markets where pressure builds silently until rules break.

Most investors fear the first and underestimate the second.

Tail risk in frontier and emerging markets

In developed markets, tail risk is usually financial through banking crises, liquidity freezes, asset bubbles.

In frontier and emerging markets, tail risk is more often institutional.

It comes from:

discretionary policy replacing rule-based governance,

contracts being suspended rather than enforced,

market access being restricted rather than repriced.

This is why Africa, in particular, teaches investors the wrong lesson.

The common narrative says Africa is risky because it is volatile. The deeper truth is that Africa is risky when institutions cannot absorb stress. More on this here.

Where institutions hold, volatility is survivable. Where they don’t, calm becomes dangerous.

The hidden form of tail risk: time

In African markets, tail risk often appears not as a crash, but as time risk.

You do not lose your capital in one dramatic moment.

You lose it slowly because:

FX is rationed,

repatriation is delayed,

contracts are renegotiated quietly,

exits become discretionary.

This is tail risk disguised as patience. By the time the loss is visible, the option to act is gone.

Why investors consistently get this wrong

If the data is so clear, why does the global market continue to misprice the continent? The answer isn't a lack of information; it’s a structural inability to process it. There are three primary reasons investors fall into the trap of "tranquil safety."

First, incentives. Career risk favours staying close to benchmarks, even when benchmarks embed tail risk. It is far safer to lose money alongside everyone else—clinging to an index that embeds hidden tail risk than it is to be right in a "noisy" market where your peers are afraid to tread.

Second, models. Most financial models are designed to measure variance—the daily zig-zags of a price—rather than rupture. We use tools built for stable, developed markets and apply them to frontiers. These models are excellent at pricing a mild storm, but they are blind to a regime break. They mistake a lack of movement for stability, failing to realize that a lack of small tremors is often what leads to the earthquake.

Third, psychology. We are hard-wired to over-weight the drama we can see and under-weight the catastrophe we cannot imagine. A protest on the streets of Nairobi is "visible" risk; it feels dangerous. A quiet centralization of power in a tranquil capital is "invisible" risk; it feels safe. History shows the opposite is often true.

What managing tail risk actually means

Managing tail risk is not about predicting the next crisis.

It is about structuring exposure so that you survive when prediction fails.

That means:

Using equity only where exits are credible.

Using duration only where institutions can support it.

Using optional structures where neither applies.

Treating calm with scepticism when it is enforced rather than earned.

In other words, it means aligning instruments with institutional reality, not political optics.

The Machiavellian lesson

Machiavelli argued that societies do not grow stronger by suppressing conflict, but by channelling it through institutions. The same logic applies to markets.

Volatility that is absorbed strengthens systems. Stability that is enforced weakens them.

For investors, that distinction is everything. It separates volatility that can be priced from risk that cannot.

That is the true meaning of tail risk.

The uncomfortable conclusion

Most investment losses in Africa do not come from being wrong about growth. They come from being wrong about institutions.

Tail risk is not the risk that markets move against you. It is the risk that markets stop being markets.

And that is why the most important question for any Africa investor is not:

How volatile is this market? But rather When stress arrives, will rules hold or will discretion take over?

That is the line between risk and ruin.

Professional overthinker. Occasional optimist. Building a platform for #InvestinAfrica - driving impact through capital, innovation, and technology.